The Netherlands Sports Betting Market: 2026 FIFA World Cup Opportunity

- Joshua Hodgson

- May 4

- 5 min read

Market Overview

The Netherlands’ legal sports betting market, across both online and retail channels, is forecast to generate approximately €2.6bn in turnover during 2026, supported by modest underlying growth in the land-

based channel and a partial recovery in online activity following a period of regulatory tightening. This positions the Netherlands as a mid-sized European sports betting market by turnover, albeit one that is materially smaller than longer-established neighbours. Football remains the dominant sport, accounting for approximately 68% of wagering activity, according to H2’s proprietary player survey data conducted in early 2026.

Based on the same survey, international fixtures represent a relatively small share of this activity, with only 7.6% of total football betting spend attributed to matches outside domestic club competitions, although this proportion is expected to rise in a World Cup year. Within this, betting remains heavily concentrated on matches involving the Netherlands, which account for approximately 80% of international football spend.

As a result, an expanded group stage with more participating teams is unlikely to materially increase overall betting activity when compared to an international tournament in the original format. Wagering on matches not involving the Netherlands is typically limited and tends to be concentrated in the later knockout stages of the tournament.

Dutch Share of Gambling Spend on Football

Source: H2 Gambling Capital, April 2026

Dutch Regulatory Context

The Dutch online market is defined by its comparatively short, regulated history. Online sports betting was licensed for the first time under the KOA Act, which came into force on 1 October 2021, under the oversight of the Kansspelautoriteit (KSA). The market channelised rapidly in its first full year of regulation, with onshore operators capturing over 60% of total sports betting turnover by 2022, before a series of policy interventions slowed and partially reversed this trend. An untargeted advertising ban took effect in July 2023, and mandatory monthly deposit limits were introduced in October 2024. Taken together, these measures contributed to a contraction in onshore activity during 2024-2025. H2 estimates that onshore channelisation by turnover eased from a peak of c.63% in 2022 to c.47% in 2025, before partially recovering to c.49% in the 2026 forecast.

This regulatory context is directly relevant to the World Cup opportunity. Major international tournaments have historically been an important customer acquisition and reactivation window for sportsbook operators, and the 2026 event is likely to represent a meaningful opportunity for onshore licensees to reclaim ground from offshore competitors.

2026 FIFA World Cup

Against this backdrop, the 2026 FIFA World Cup is expected to act as a key near-term catalyst. FIFA has projected that up to six billion people will engage with the tournament in some form, making it the most-watched sporting event in history. For Dutch sportsbook operators, this translates into a potential material uplift in handle, customer acquisition, and broader engagement metrics - with the precise revenue impact ultimately shaped by match outcomes and the success of the Dutch team in the tournament.

The timing of the tournament enhances its potential impact. Taking place across June and July, the World Cup falls during what is typically the quietest stretch of the footballing calendar, when the Eredivisie, UEFA competitions and the other major European leagues are in their summer break. This stands in sharp contrast to the 2022 Qatar edition, which was staged in November and December - a period already rich in domestic and European fixtures. The result was that the prior World Cup did little to augment what would have been a busy period anyway; the 2026 edition, by contrast, arrives during a natural lull and should generate incremental volume that would otherwise not exist.

The tournament’s expanded format adds a further dimension. For the first time, 48 nations will compete rather than 32, producing 104 matches in total - 40 more than any previous World Cup. This increase in fixture volume directly expands the addressable betting opportunity, providing operators with a substantially larger event slate on which to drive engagement.

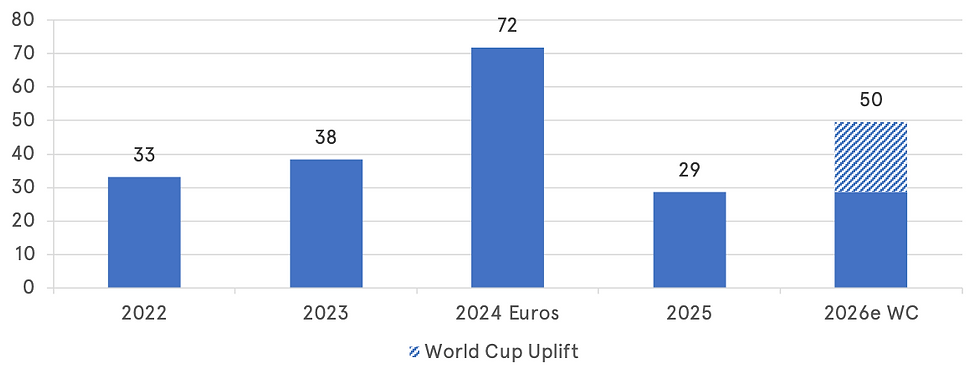

Historical data offers a compelling illustration of what major football tournaments can do to Dutch betting volumes. In 2024, the Netherlands reached the semi-finals of UEFA Euro 2024, providing a useful summer-tournament benchmark without the complicating factor of home-nation hosting. Combined Dutch online sports betting gross win for June and July that year rose 88% relative to the same period in 2023, and was more than double the equivalent summer months in 2025. The 2025 comparison should, however, be read with caution: the introduction of monthly deposit limits in October 2024 materially dampened onshore activity across 2025 as a whole, and therefore flatters any year-on-year comparison with tournament periods.

As previously noted, the 2026 World Cup will feature more than double the number of matches played at the Euros and will carry a greater global prestige. It is, however, prudent to approach projections of potential growth with caution. A significant portion of these matches will occur at times less favourable for European audiences given the US/Canada/Mexico host venues, and while the expanded format generates more fixtures, it may dilute interest in individual games, potentially impacting perceived quality and diminishing the sense of occasion for spectators.

Combined June & July Dutch Online Legal Sports Betting Gross Win (€m)

Source: H2 Gambling Capital, April 2026

Historical comparisons prior to 2022 are constrained by the absence of a regulated onshore online market in the Netherlands; monthly series are only available from the first full post-KOA year. For external context, France’s national gambling authority (ANJ) reported that online stakes on the 2024 Euros were 27% of total sports stakes over the June / July period, but the Euros have a lower impact to that of the World Cup. For the World Cup 2022, we estimate that the World Cup stakes were c.35-40% of the November / December sports betting stakes for the French online market – but this is a busier period for sports than a summer World Cup. However, both of these provide cross-market evidence of the scale of uplift a major tournament can generate in a comparably regulated European market.

Potential Impact on Dutch Market

Considering all of this, H2 expects a boost of c.€180m to turnover attributable to the upcoming World Cup. This equates to c.7.0% of predicted annual 2026 legal sports betting turnover, consistent with the figure applied for the German market and broadly aligned with data from France regarding the 2022 World Cup, which saw 7.2% of annual sports betting turnover spent on the competition. In that tournament, France saw a gross win margin of 11.73%, with operators also citing favourable results. If a similar margin is achieved in the Netherlands, it would equate to an implied gross win boost for the legal Dutch market of c.€21.1m.

The scale of this uplift will depend particularly on the Dutch national team’s progression through

the tournament. The Euro 2024 comparison illustrates how responsive Dutch wagering is to its own team’s engagement, with a semi-final run producing a materially higher summer than in a normal non-tournament year. An early exit at the 2026 World Cup would compress the uplift accordingly, while a deep run into the knockout stages would be expected to push handle towards, or above, the upper end of the benchmarks above. The deposit-limit regime introduced in October 2024 is a second variable worth monitoring: it represents a downside risk to per-customer peak-event stakes relative to previous tournaments.

Comments